Summary

- Shipping rates have declined significantly in 2022 with dry bulk rates down as much as 89% and container rates down as much as 45%.

- Sea freight shipping rates are an indicator of economic conditions due to inelastic supply.

- Lower shipping rates are suggesting lower inflation and further weakness in equity markets including the materials sector and emerging markets.

One of my preferential leading economic indicators is global sea freight shipping. This is because sea freight is a strong indicator of global economic growth. Every developed nation relies on goods that are shipped at sea and the types of goods shipped at sea are widespread including raw materials including grains, metals, crude oil, natural gas, and manufactured products including vehicles and semiconductors.

Sea freight shipping is a reliable indicator because the supply of shipping is relatively inelastic. The construction of freight ships requires years of manufacturing, therefore shipping rates will generally respond faster to changes in demand.

In 2021, shipping rates exploded to unbelievable heights. The story is quite different in 2022 with rates now falling back to Earth. This shift in momentum is an economic signal. It is a shot across the bow for markets.

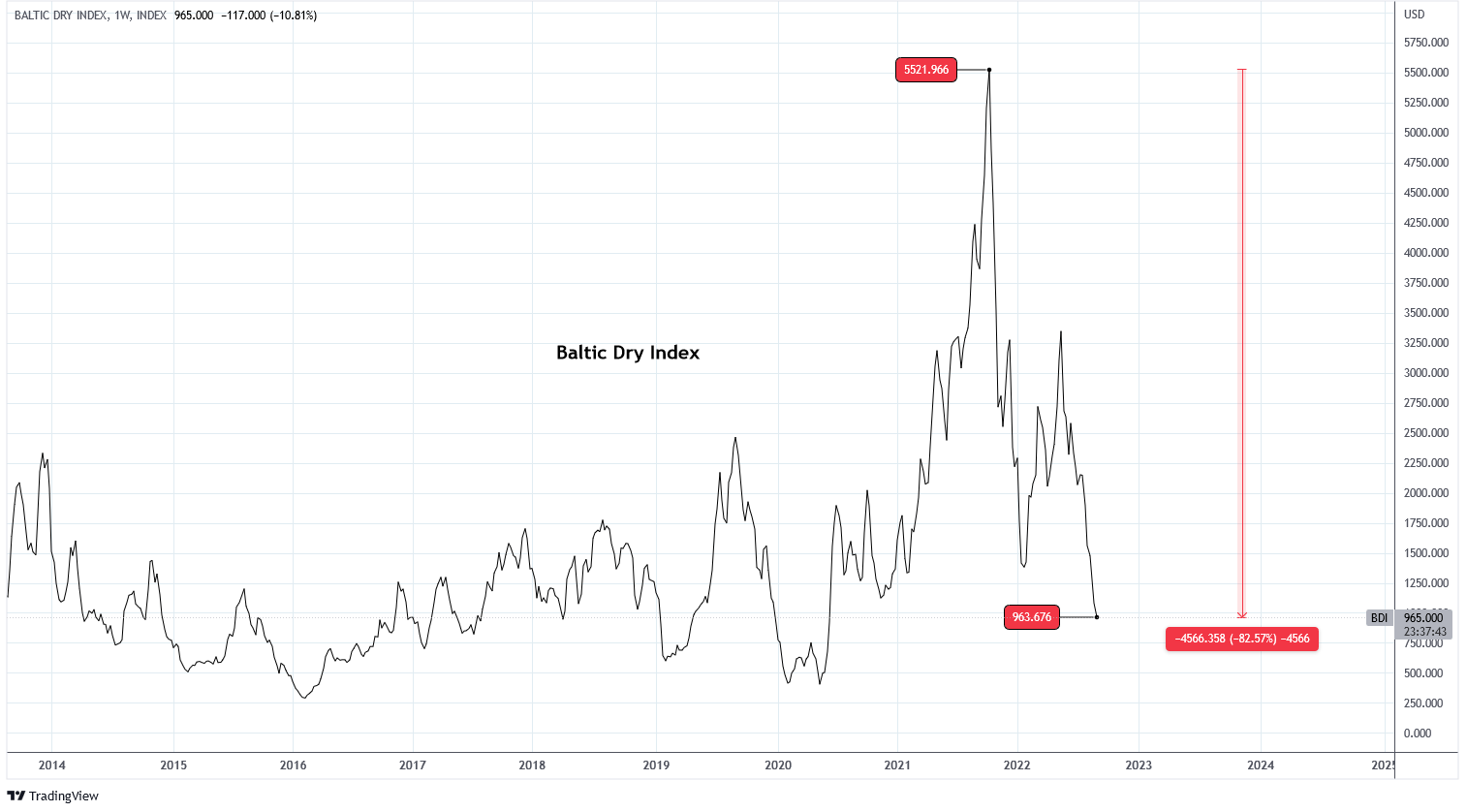

Shipping Is Sinking

Shipping rates have been in decline in 2022 and are beginning to retrace the post-pandemic climbs. The Baltic Dry Index is a composite index of dry bulk rates around the globe and represents the overall cost of dry bulk shipping goods including coal, grains, fertilizers, and metals. The BDI has fallen 82% from 5,521 to 963 in less than a year. This implies that global demand for dry bulk goods is easing and the cost of shipping, which is embedded in the cost of products sold to consumers and therefore price inflation, is now much lower than it was a year ago.

{kind=link}

Charts by TradingView (adapted by author)

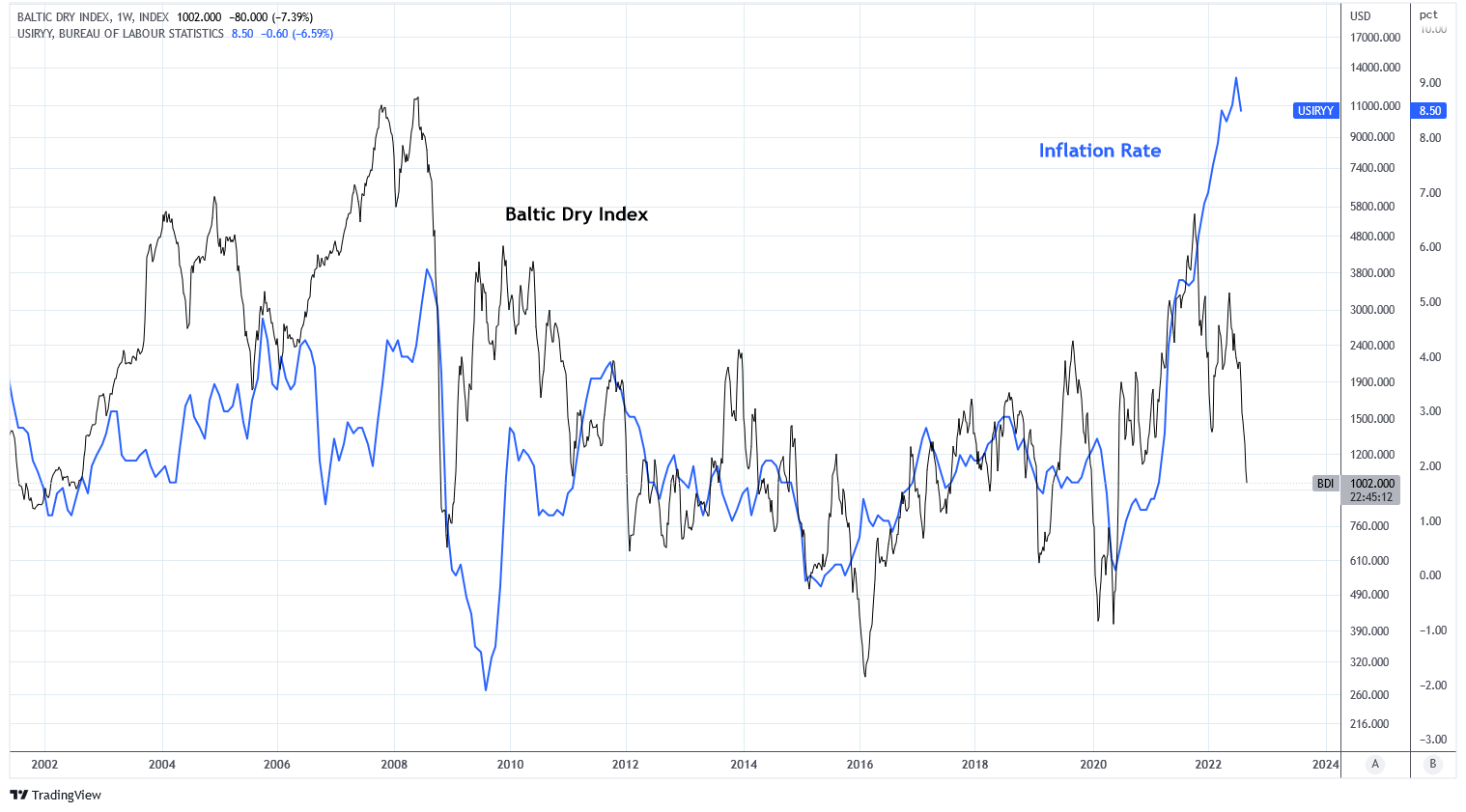

The next chart shows the correlation between the BDI and U.S. inflation rate. The BDI often leads inflation and the current trend is much lower with a wide divergence between the index and CPI.

{kind=link}

Charts by TradingView (adapted by author)

The BDI includes rates for Capesize, Panamax, and Supramax cargo vessels. According to Greg Miller of American Shipper, the average Capesize rate has fallen from approximately $80,000 to $8,783 per day from October 2021 to today. That is now lower than the 5-year low for this time of year. Panamax and Supramax rates are near their 5-year averages.

Rates for dry bulk shipping has declined more dramatically than container rates, so far. The Drewry Spot Index determined that the spot rate for container shipping from Shanghai to Los Angeles declined 23% YoY in July. The Drewry World Container Index has declined 45% since last September.

{kind=link}

The Daily Shot (used with permission)

Volumes are Sustaining For Now

According to data from Descartes, U.S. container import volumes in June were lower than May but the highest seasonal volume since 2019. Twenty foot equivalent (TEU) volumes are 26% higher than in 2019 before the pandemic at 2,480,946. The average port delay across the top ten U.S. ports declined by 7% from May to June 2022 but the number of ships waiting off U.S. coasts for loading has risen by 66% since June. Additionally, the Suez Canal recorded an all-time high in daily traffic in August.

While volumes are sustaining for the moment, the trend in volumes has been decreasing as represented by the Baltimore/Charleston/Virginia total volume port guidance which is showing negative YoY activity in 2022.

The Daily Shot (used with permission)

Economic Implications

The shift in trend for shipping rates is signaling a change in economic growth that will impact markets. Falling shipping rates implies both lower economic activity and lower inflation.

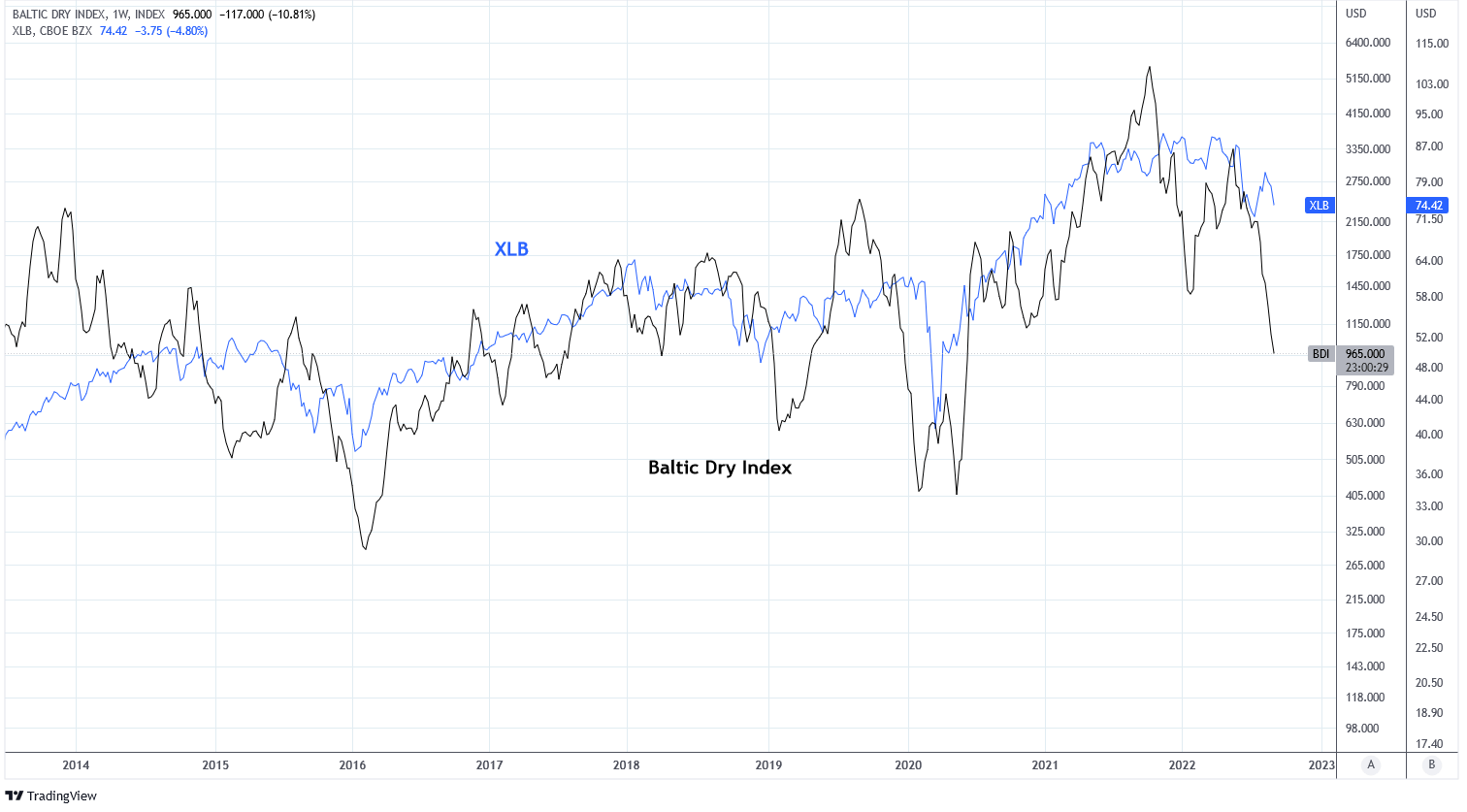

Among the sectors that will experience disruptions as forecasted by shipping includes the Materials Sector represented by XLB. Materials and BDI are correlated as materials equities produce and sell dry bulk goods. Currently the BDI is forecasting a substantial decline in XLB.

{kind=link}

Charts by TradingView (adapted by author)

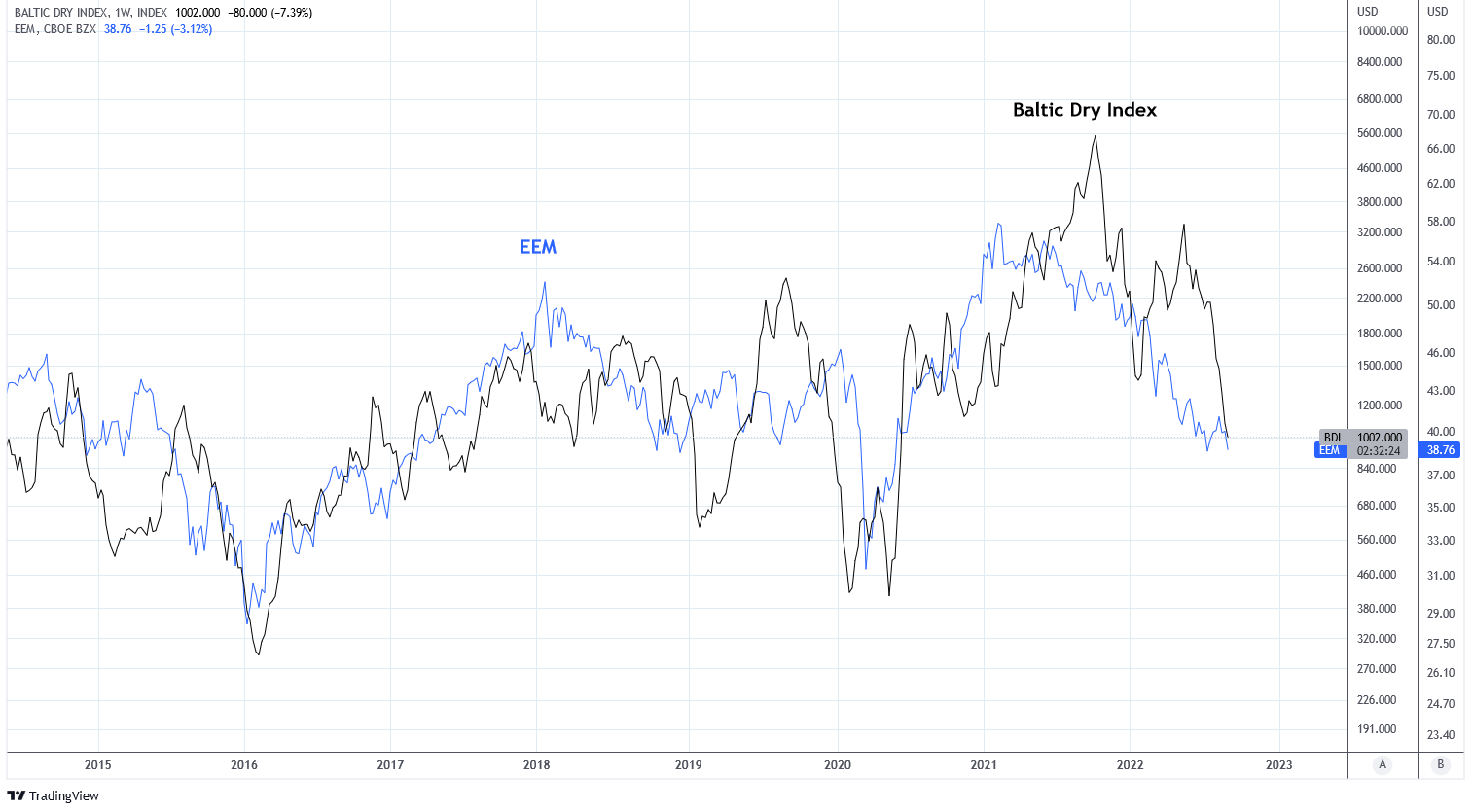

Another sector that is particularly vulnerable to less demand for dry bulk goods is the emerging markets, represented by EEM. Emerging market economies often rely on income from dry bulk goods they produce. Currently, emerging market equities have corresponded with the fall of the BDI, primarily because of U.S. dollar strength, but will continue to follow the BDI if it continues lower, which I think is likely given macroeconomic conditions.

{kind=link}

Charts by TradingView (adapted by author)

Sea freight shipping is an excellent source of information for forward-looking economic conditions. The cost of shipping surged higher in 2021 along with inflation. Shipping rates have now fallen significantly and are forecasting weaker economic conditions and lower inflation. Shipping volumes have sustained for now but I am expecting volumes to decrease over the coming months. The signal is not supportive of many markets including general equities and especially the materials sector and emerging markets.